Flood Insurance Program Faces September Deadline, With Florida Most at Stake

The National Flood Insurance Program, the federal backbone of flood coverage for millions of American homeowners, faces a reauthorization deadline at the end of September, and no state has more riding on the outcome than Florida. With its extensive coastline, low-lying geography, and vulnerability to hurricanes and flooding, Florida is home to a large share of the nation's flood insurance policies, making the program's fate a matter of direct consequence for hundreds of thousands of residents.

The program, commonly known by its initials NFIP, was extended earlier in the year through legislation that set its authorization to expire on September 30. Congress must act again before that deadline to reauthorize the program, or risk a lapse that could disrupt the flood insurance market at a particularly sensitive time, during the heart of hurricane season. The recurring nature of these deadlines has become a familiar source of anxiety for property owners and the real estate industry, who have watched the program pass through a long series of short-term extensions rather than a lasting resolution.

How the program works

The National Flood Insurance Program was created because private insurers have historically been reluctant to offer flood coverage, given the catastrophic and correlated nature of flood losses. Unlike risks that are spread thinly across many unrelated policyholders, a single flood can damage thousands of properties at once, concentrating losses in a way that private carriers have long found difficult to absorb. The federal program fills that gap, providing flood insurance to property owners in participating communities and making coverage available where the private market often will not.

Flood insurance is separate from standard homeowners insurance, which typically excludes flood damage. Many property owners are surprised to learn that the policy protecting their home against wind, fire, and theft offers no protection against rising water, a distinction that becomes painfully clear after a storm. For properties in designated high-risk flood zones with federally backed mortgages, flood insurance is mandatory, meaning the availability of coverage through the program is essential for many homeowners to satisfy their loan requirements and protect their property.

The program must be periodically reauthorized by Congress, and over the years it has been extended numerous times, sometimes on short-term bases that create uncertainty. A lapse in authorization can prevent the program from issuing new policies or renewing existing ones, which can complicate home sales and leave property owners in limbo, particularly in flood-prone regions. Even the possibility of a lapse can inject caution into the market, as buyers, sellers, and lenders weigh whether coverage will be available when they need it to close a transaction.

Participation in the program also comes with obligations for local governments, which must adopt and enforce floodplain management standards in exchange for access to federal coverage. Those standards, covering how and where structures may be built in flood-prone areas, form part of the broader framework the program uses to reduce risk over time, tying the availability of insurance to community-level efforts to build more safely.

Why Florida has the most at stake

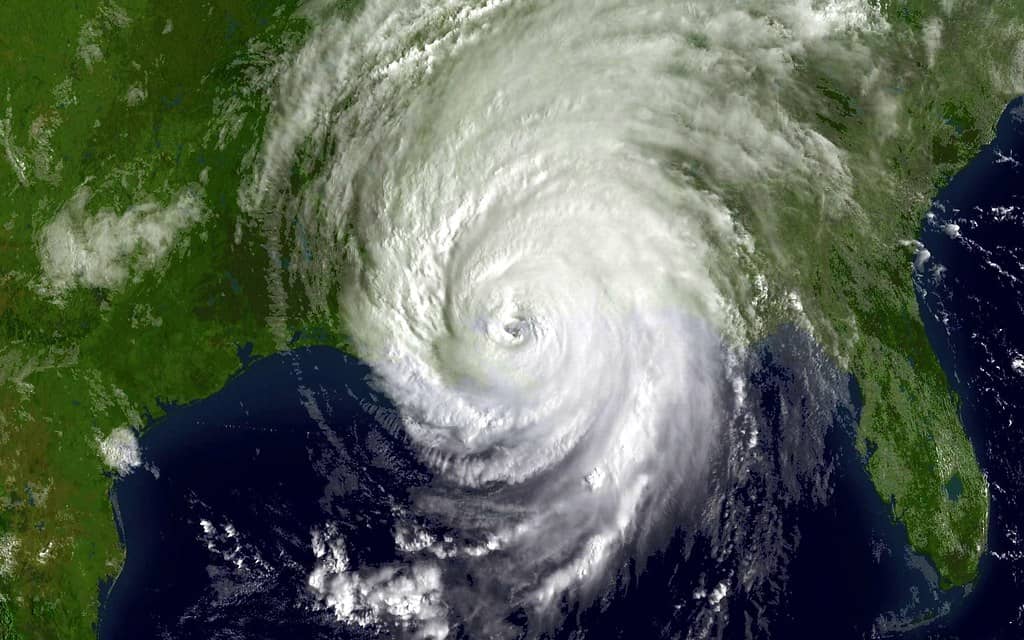

Florida's exposure to flooding is unmatched among the states. Its long coastline, flat terrain, high water table, and frequent exposure to hurricanes and heavy rainfall make flood risk a pervasive reality across much of the state. As a result, Florida accounts for a substantial portion of all flood insurance policies in the country, giving it an outsized stake in the program's continuity. Flooding in Florida is not confined to the coast, as the state's low elevation and heavy seasonal rains can send water into neighborhoods far from the shoreline.

A disruption to the flood insurance program would ripple through Florida's housing market, where flood coverage is a prerequisite for many transactions. Home sales that require flood insurance could be delayed or derailed if the program cannot issue new policies during a lapse, adding friction to a market already strained by affordability challenges. Real estate agents, title companies, and lenders across the state depend on the program's steady operation to move transactions to closing, and any interruption would be felt quickly.

The timing of the deadline heightens the stakes. September falls within the most active portion of the Atlantic hurricane season, when the threat of flooding is at its peak. A lapse during that window would be especially concerning for Florida homeowners, who rely on flood coverage precisely when storms threaten the state. The convergence of the reauthorization deadline and the season's most dangerous stretch gives the issue an urgency that is difficult to overstate for residents in harm's way.

The broader insurance context

The flood insurance question intersects with Florida's broader property insurance challenges. The state has grappled with a difficult homeowners insurance market in recent years, marked by high premiums and carrier instability, though there have been signs of stabilization more recently. Flood coverage, provided largely through the federal program, is a distinct but related piece of the overall picture of protecting Florida properties. For many households, the flood policy and the homeowners policy together represent a significant and growing share of the cost of keeping a roof overhead.

The reliance on a federal program for flood coverage reflects the limits of the private market in handling catastrophic flood risk. Efforts to encourage private flood insurance have grown, but the federal program remains the dominant source of coverage, particularly for the high-risk properties that need it most. Its reauthorization is therefore central to the stability of flood protection in the state. Where private options do exist, they often build upon or compete at the margins of a market whose foundation is still the federal program.

The financial structure of the program has long been a subject of debate, as it has accumulated significant debt from major flood events. Discussions about reforming the program, updating its rate-setting to better reflect risk, and addressing its long-term solvency have accompanied past reauthorizations, and those issues remain part of the backdrop as the deadline approaches. Efforts to align premiums more closely with actual risk have proven contentious, as changes that improve the program's finances can also raise costs for the very homeowners who depend on it most.

What it means for Floridians

For homeowners, the program's reauthorization is essential to maintaining access to affordable flood coverage. A lapse could prevent the issuance of new policies and complicate renewals, creating uncertainty for those who depend on flood insurance to protect their homes and satisfy mortgage requirements. Households in flood zones plan their finances around the assumption that coverage will be available, and disruption to that assumption can leave them exposed at the worst possible moment.

For prospective homebuyers, the availability of flood insurance affects the ability to close on properties in flood zones. A disruption to the program could stall transactions, adding to the challenges buyers already face in Florida's high-cost housing environment. The interplay of flood coverage and home sales makes the program's continuity a practical concern for the market. A buyer ready to purchase can find the process frozen if a required flood policy cannot be issued, delaying moves and unsettling the chains of transactions that depend on one another.

For the state as a whole, the program underpins the financial protection of a vast number of properties against a risk that is central to Florida life. Ensuring its continuity supports the resilience of communities across the state, from coastal cities to inland areas prone to flooding during heavy rains and storms. When flooding strikes, the ability of families and businesses to rebuild often hinges on whether they carried coverage, making the program a quiet but essential part of the state's capacity to recover from disaster.

Lenders, too, have a stake in the program's continuity, since the mortgages they hold on properties in flood zones are protected in part by the requirement that borrowers carry flood coverage. A lapse that prevents new policies from being written can complicate not only sales but also the routine functioning of the mortgage market in flood-prone areas, adding a layer of uncertainty to transactions that would otherwise proceed smoothly.

The stakes of a lapse

A lapse in the program does not erase coverage that is already in force, but it can halt the issuance of new policies and interrupt the machinery that keeps the flood insurance market moving. During past interruptions, the inability to write new coverage created bottlenecks in real estate transactions, as buyers in flood zones were unable to obtain the policies their lenders required to close. In a state where flood coverage is woven into so many sales, even a brief interruption can have outsized effects.

The uncertainty surrounding repeated short-term extensions also imposes costs that are harder to measure. Property owners, insurers, and local officials must plan around the possibility of disruption, and the lack of a long-term resolution complicates the kind of forward planning that flood resilience requires. For Florida, where the exposure to flooding is a permanent feature of life rather than an occasional concern, the value of a stable and predictable program is difficult to overstate.

What's next

Attention now turns to Congress, which must reauthorize the program before the September 30 deadline to avoid a lapse. Lawmakers have repeatedly extended the program in the past, often as part of broader legislative packages, and a similar path is possible again, though the timing and terms remain to be determined. The pattern of last-minute action has become a recurring feature of the program's history, leaving stakeholders to watch the legislative calendar closely as the deadline nears.

For Florida, the outcome carries significant weight, and the state's congressional delegation and officials are likely to press for continuity given the program's importance to their constituents. As the deadline approaches during hurricane season, the reauthorization of the National Flood Insurance Program stands as a consequential piece of federal business with direct implications for the state most exposed to the risks it covers. Whether Congress delivers a clean extension, a broader reform, or another short-term stopgap, the decision will shape the flood protection available to millions of Floridians at a moment when the threat of high water is most acute.

Spotted an issue with this article?

Have something to say about this story?

Write a letter to the editor